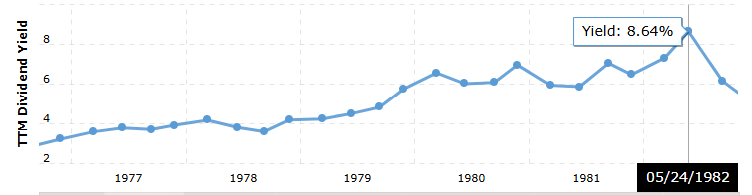

Back in the day, you could park your cash in a stock and yield hefty 8% dividend checks…

Giving you capital gains and cash flow to offset rising costs.

A standard $250k retirement account would’ve seen healthy market returns.

But in today’s market… you’re lucky to get much more than 1% in dividends.

So chasing dividends might look like a dead game… if you don’t know a smarter way to find solid stocks.

Picking the right stocks keeps you on the right track…

And gives you more shots to reap returns over time.

That’s why I had to get these 5 dividend-investing cheat sheets to you.

After more than a decade trading the markets, and having contacts which include a former hedge fund manager, a trading champion, and a former bank VP…

I believe everything you’ll see inside will give you a special look at how to go after dividend stocks.

You’ll get to see every single detail I look for before I even touch any stock for dividends…

In fact, you’ll get the two dividend stocks I personally put $50,000 of my own money into.

No reckless guarantees when it comes to trading, of course.

But before you load up on another dividend stock next…

Check out these cheat sheets… free.

By clicking the link above you agree to periodic updates from ProsperityPub and its partners (privacy policy)

GitLab Sell-Off Overdone: AI and Cash Flow Signal a Rebound

Author: Thomas Hughes. Date Posted: 3/4/2026.

Key Points

- GitLab is well-positioned for the age of AI inference, as it enables superior outcomes at all stages of the software development lifecycle.

- Tepid guidance and a weak analyst response sent shares to long-term lows, where institutions are likely to buy.

- Cash flow is king in 2026, and GitLab has it, as evidenced by its inaugural $400 million share buyback authorization.

- Special Report: [Sponsorship-Ad-6-Format3]

Fears of slowing growth and AI disruption sent GitLab (NASDAQ: GTLB) shares to multi-year lows in early March. That sell-off, already overdone, has pushed the stock into ultra-deep value territory and presents an attractive buying opportunity.

While AI-related concerns are weighing on the near-term outlook, GitLab continues to grow and is well-positioned for the AI inference era. Its platform—and newer products—embed AI functionality across the software lifecycle, improving efficiency and outcomes while preserving security, compliance and governance controls.

Have $500? Invest in Elon's AI Masterplan (Ad)

What if you could claim a stake in what's set to be the biggest IPO ever… starting with just $500?

Everyone is talking about Elon Musk's SpaceX IPO.

Evidence of its positioning and outlook appears in its cash flow and balance sheet, which supported the authorization of a share buyback. The company is cash-flow positive despite aggressive investment, expects continued improvement, and plans to repurchase up to $400 million of shares.

That buyback represents about 10% of the post-release market cap, reinforcing an already-solid support base. Investors can reasonably expect GitLab to buy stock on price pullbacks, such as the early-March decline that pushed shares to record lows.

The balance sheet shows a strengthening capital position and improving shareholder value. Current assets rose across categories at year-end, with cash and equivalents well above liabilities. The company carries no long-term debt, total liabilities are less than equity, and equity increased 27% for the year.

Valuation, Institutions, and Analysts Point to GTLB's Robust Upside Potential

On the basis of consensus earnings estimates, GitLab's shares could double from their March lows. Forecasts imply a high‑teens to low‑20% compound annual growth rate (CAGR) through the middle of the next decade, which would put the stock near ~10x its 2035 consensus. In one scenario, the stock could rise at least 100% to align with broad market averages, or 200%+ to approach established blue‑chip tech multiples.

GitLab's value is also reflected in institutional and analyst trends. Institutions—including public and private funds—own roughly 95% of the float and have been accumulating shares.

MarketBeat data show institutions have been net buyers for 13 consecutive quarters, with buying activity accelerating in 2025 and again in early 2026.

That creates a meaningful support base likely to remain a tailwind for the stock once a rebound gains traction in 2026.

Analysts reacted cautiously to GitLab's fiscal Q4 2026 report, although that was against a high bar. MarketBeat tracked six immediate rating actions within 12 hours of the release: one downgrade, five price-target reductions and one affirmation. Despite those moves, sentiment trends shifted little.

Those six ratings represent a slightly stronger profile than the broader "Moderate Buy" consensus. The revised price targets sit at the lower end of the range but average just below the wider consensus, implying roughly 65% upside potential.

GitLab Offers Mixed Guidance After Strong Report

GitLab delivered a solid fiscal 2026 (FY2026) and Q4. The company reported $260.4 million in net revenue, up 23.2% year over year and about 320 basis points ahead of consensus. Strength was led by larger customers: overall customer counts rose roughly 8%, driven by an 18% increase in large customers and a 26% gain in mega-sized customers. Net retention rate (NRR), a key penetration metric, was strong at 118%. Forward-looking remaining performance obligation (RPO) also rose—up 24% on a current basis and 20% overall—supporting expectations for continued growth.

Margin developments were encouraging. While gross margin compressed by 200 basis points, improvements in operating efficiency more than offset that decline. Adjusted operating margin improved by 300 basis points, contributing to a 42.8% increase in operating income. The offsetting negative was higher spending, which reduced adjusted EPS and free cash flow year over year. Still, adjusted EPS of $0.30 beat forecasts by $0.07, providing little reason for a sell-off.

Guidance was mixed versus consensus but fundamentally solid. Revenue guidance modestly missed expectations while earnings guidance was stronger. The company expects revenue growth north of 17% this fiscal year and wider margins, with adjusted EPS guidance roughly 250 basis points above consensus. Management outlined initiatives to drive growth—expanding go‑to‑market capacity, accelerating client acquisition, optimizing pricing and packaging, and executing its AI strategy.

Why eBay's Depop Acquisition Matters More Than the Earnings Beat

Author: Chris Markoch. Date Posted: 2/20/2026.

Key Points

- eBay’s Q4 beat and GMV acceleration support a comeback narrative, even as the stock remains pressured by broader “AI trade” sentiment.

- Advertising and recommerce are emerging as durable growth engines, while Depop adds a targeted Gen Z/Millennial wedge.

- Depop integration costs, cyclical category tailwinds, and margin pressure remain the main risks to watch.

- Special Report: [Sponsorship-Ad-6-Format3]

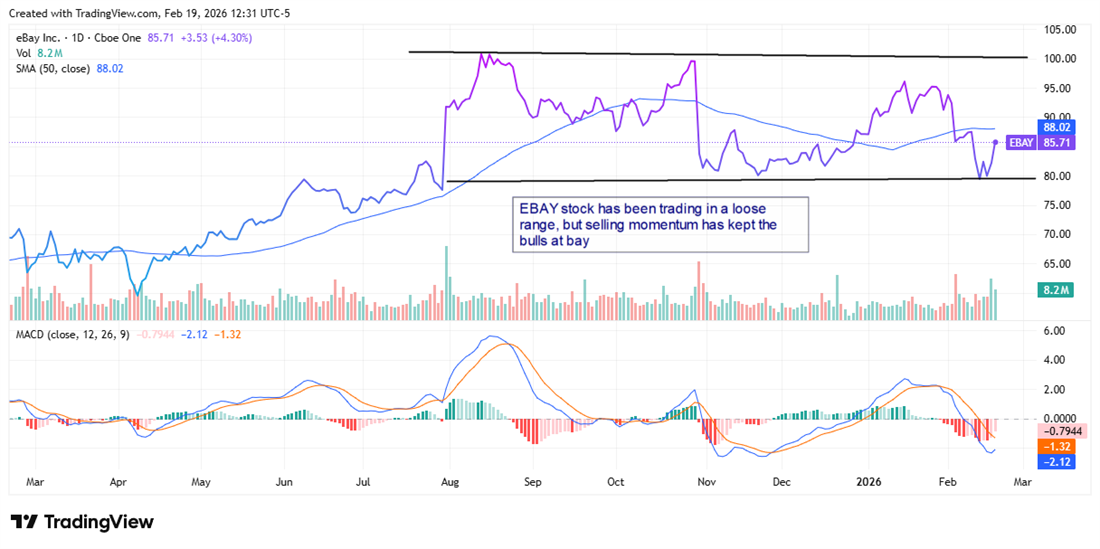

Shares of eBay Inc. (NASDAQ: EBAY) are up about 3.8% the day after the company delivered a strong Q4 2025 earnings report. On one level, the report makes sense: the company is a pure play on consumer spending, which has remained resilient despite conflicting macroeconomic data. Plus, eBay fits into the "discount" category of retail stocks, which has performed well in a volatile market.

There was much for investors to like in the report. Revenue of $2.97 billion beat expectations of $2.87 billion. Gross merchandise volume (GMV), a key metric, climbed to $21.2 billion — up almost 6% globally and nearly 10% in the United States — suggesting the platform is expanding and attracting more customers.

This makes me furious (Ad)

I Called Black Monday. Now I'm Calling March 26!

I predicted the 1987 crash six weeks early. I called the fall of the Berlin Wall. I pinpointed the exact bottom in 2009.

Now I'm staking my reputation on March 26, 2026 - the day I believe Elon will announce the SpaceX IPO.

Bloomberg is calling it "the biggest listing of ALL TIME."

A $1.5 TRILLION valuation... the "wealth-building" moment of the decade.

Today, I'll show you how to get in before the big announcement.

Another notable development was the announcement that eBay will acquire Depop, the secondhand clothing marketplace owned by Etsy Inc. (NASDAQ: ETSY), for $1.2 billion in cash. The deal is a strategic effort to capture more of the Gen Z and Millennial customer base.

Like many stocks with even minimal exposure to artificial intelligence (AI), EBAY was trading lower in 2026 ahead of the report. One strong quarter won't erase that trend, but there are several reasons to believe in eBay's comeback.

Ads, Fashion, and the Recommerce Angle

The Q4 results highlighted three specific growth engines. First is advertising. On an annualized basis, eBay is approaching $2 billion in ad revenue — a line of business that was almost non-existent five years ago.

Total advertising revenue was $544 million in Q4, representing GMV penetration of nearly 2.6%, with first-party ads growing over 17% to $517 million. About 4.8 million sellers adopted at least one promoted listing product during the quarter. The takeaway: advertising is becoming an embedded behavior on the platform, not just an optional tool for power sellers.

The second engine is recommerce (pre-owned and refurbished merchandise). This category accounted for over 40% of the company's GMV in 2025 and grew roughly 10% during the year. Recommerce is an area where eBay is distinct from Amazon.com Inc. (NASDAQ: AMZN), and one Amazon will be hard-pressed to replicate at scale.

The third growth driver is the Depop acquisition. In 2025, Depop generated about $1 billion in gross merchandise sales for Etsy, and nearly 90% of its 7 million active buyers are under age 34 — a demographic eBay has struggled to attract. Depop's focus on fast-growing private-label and vintage fashion could help eBay establish a stronger foothold with younger shoppers and drive incremental revenue if those users migrate to eBay's platform.

A Marketplace Revamp With Real Teeth—or Temporary Tailwinds?

Institutional sentiment on EBAY has been bearish over the last three quarters, with selling outpacing buying by roughly $2 billion. Some of that selling followed the stock's rally to an all-time high in August 2025. Since then, EBAY has traded in a loosely defined range with support around $80 and resistance near $100.

Nonetheless, eBay analyst forecasts on MarketBeat show analysts have been quick to raise price targets on EBAY. Several of the new targets are above the consensus price of $96.52 — roughly 12% higher than the stock price at the time of writing. The highest target comes from Needham & Company, which raised its price target to $122 from $115.

Investors should also consider the company's dividend. A dividend alone shouldn't be the primary reason to buy EBAY; investors should prefer companies that are also investing in growth, as eBay is with the Depop deal.

Still, the dividend yield of 1.35% is above the S&P 500 average. eBay has increased the annual dividend to $1.16, an average rise of more than 14% over the past three years. The payout ratio sits at just over 25%, which appears sustainable and not unduly draining cash.

Risks That Investors Shouldn't Ignore

There are several risks to weigh. First, some of Q4's GMV growth was commodity-driven. Management noted on the earnings call that bullion, collectible coins, and Pokémon trading cards provided meaningful tailwinds in late 2025 — categories that are cyclical and unlikely to repeat at the same rate.

Second, the Depop acquisition, while strategically sensible, carries near-term costs. eBay expects the deal to be a low single-digit headwind to non-GAAP operating income growth and to dilute EPS growth in the short term, with accretion not anticipated until 2028.

Third, non-GAAP gross margin slipped by nearly 80 basis points year over year. Sustainable margin expansion in the face of Amazon's logistics network and Shopify's (NASDAQ: SHOP) seller ecosystem remains a central challenge. The margin decline was primarily driven by scaling managed shipping and Authenticity Guarantee programs — necessary investments that underscore the real costs of maintaining trust on a peer-to-peer marketplace.

Bottom line: eBay's Q4 beat and the Depop deal provide clear paths for growth — ads, recommerce, and access to younger shoppers — but investors should balance that upside against commodity-driven tailwinds, near-term dilution from acquisitions, and ongoing margin pressures. Long-term gains will depend on execution.

This message is a sponsored email provided by ProsperityPub, a third-party advertiser of MarketBeat. Why did I get this email content?.

If you need assistance with your newsletter, please feel free to email our South Dakota based support team at contact@marketbeat.com.

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

Copyright 2006-2026 MarketBeat Media, LLC.

345 North Reid Place, Suite 620, Sioux Falls, SD 57103-7078. United States of America..

Comments

Post a Comment